10 Essentials Tips for Effective Debtor Management

By Paolo, 02.03.2026

Businesses that operate in specific industry sectors face the challenging, yet essential task, of managing debtors. For these businesses, this is the only way to safeguard their survival.

Debtor management isn’t just an accounting task, it’s a constant battle for healthy cash flow, making it a vital part of the business daily operations. Good quality debtors grant timely cashflow essential to pay wages, tax and creditors, and strengthening the business’ financial position when needing capital assistance for business growth.

While profitable sales may show a healthy business in the Profit & Loss, uncollected debts directly drain cashflow, creating a dangerous paradox where a business can appear profitable while being completely illiquid.

Businesses with poor cash flow often push their creditors’ payment terms to the limits, spoiling the relationships with their suppliers and being reduced with COD (Cash on Delivery) only terms, strapping their cash flow issues even further.

Poor debtor management may also have a direct impact on paying tax liabilities like GST and Income Tax for those businesses that report tax on an accrual basis, as these liabilities are due for payment irrespective of the invoices’ payment status.

The ultimate failure comes when an overdue invoice turns into a Bad Debt. This doesn’t just hit the bottom line, a bad debt is much more than a simple “write off” expense representing missed profit, it costs money and resources to make a sale and these costs are unrecoverable.

A single large bad debt can place an entire business at risk. As most small businesses target an operating profit of 10–15%, a bad debt exceeding that margin doesn’t just hurt, it wipes out an entire year’s profit, turning even a hard-earned successful year into a loss.

As prevention is better than curing, effective Debtor Management starts right from client onboarding. This blog article breaks down every phase of the Sales > Payment > Receivables cycle to ensure sound Debtor Management is integrated at every step.

Let’s be honest: chasing payments is a stressful, time-consuming chore that most business owners dread. Therefore, a major focus of this blog is automating as many of these tasks as possible. You might be pleasantly surprised to discover that many of these time-saving features are already available in Xero and MYOB.

Is Debtor Management an imperative process for all businesses?

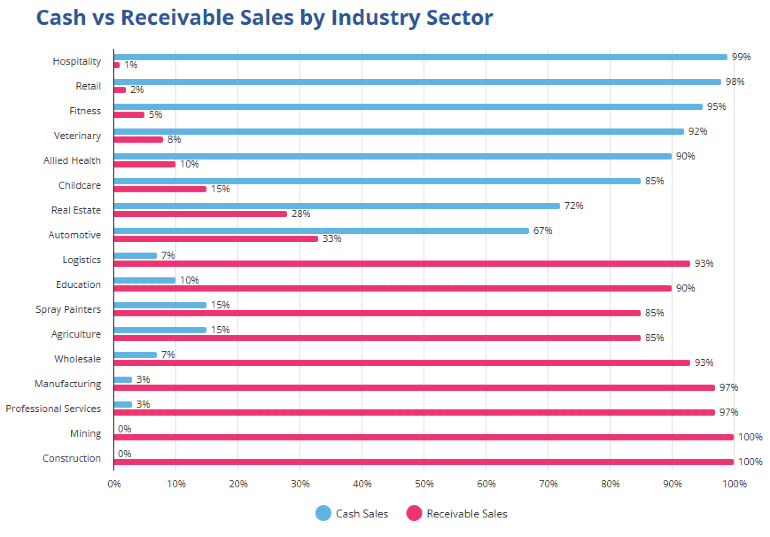

Failure to obtain payment for services rendered or goods delivered impact all business’ cashflow. However, the implementation of an effective Debtor Management process becomes more significant in those sectors when the ratio of Receivable Sales is higher than Cash Sales.

To navigate this, it is vital to understand the difference between these two sales types.

- Cash Sales > these are sales where the payment is received at the same time of the sale (no matter what payment type is used);

- Receivable sales > these are sales where payment is expected upon set payment (or credit) terms (7, 14, 30 days, end of month etc.). When the sale is issued and not paid, the outstanding sits in an Asset account called ‘Accounts Receivable’. The customer effectively becomes a ‘Debtor’ until the full invoice payment is made.

Therefore, in sectors where payment terms are the norm, a sound Debtor Management system is paramount for business survival.

Summary graph of Cash Sales versus Receivable Sales by Industry Sector

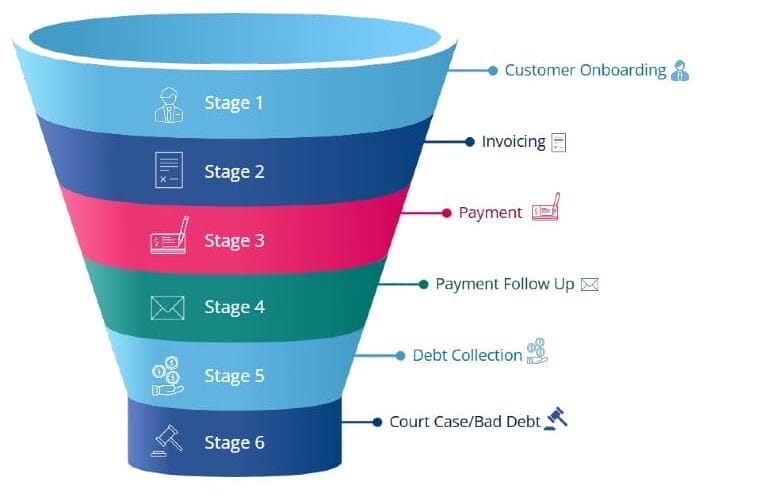

Integrating Debtor Management across each stage of the Receivable Sales Process

Debtor Management cannot just be a ‘panicked afterthought’ once a sale becomes overdue, it should be perceived as an essential preventative and responsive system, fully integrated with the Sales & Payment Process.

The Receivable Sales & Payment process includes six stages:

Sales & Payment Debt Recovery

1. Customer Onboarding 4. Payment follow-up

2. Invoicing 5. Debt Collection

3. Payment 6. Court Case/Bad Debts

- Stages 1 to 3: Debtor Management is a preventative measure designed to ensure your sales are paid as soon as possible.

- Stages 4 to 6: Debtor Management becomes a recovery process designed to attempt to recuperate either all or part of the overdue payment before it becomes a Bad Debt.

Stage 1: Customer Onboarding

Depending on the nature of the sale, customer onboarding may take place prior to the quoting or invoicing stage. This process is a fundamental step to ensure your business gathers all the required customer information, provides clear information about credit terms and conditions and ensure the customer they are engaging with is reputable.

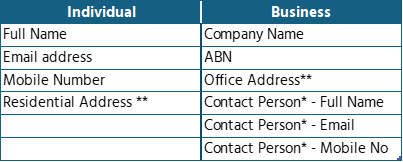

Tip #1 – Gather all customer details

Collect exhausting client information is paramount, not only from a compliance standpoint, but also to ensure a seamless customer service workflow when selling your goods or services. Finally, this is your first important step to start your Debtor Management process.

There are two types of customers: individuals and businesses. Based on the customer type, you will need to collect different details:

* when you engage with a business, you may have to collect details for multiple people working within the same organisation. This could be the procurement officer, project manager etc. Ensure you always collect the details of the person responsible to approve your invoices and payments.

** always request a physical address from your customers. Do not just accept P O Boxes.

Tip #2 – Include Terms of Payment and Engagement as part of Onboarding

The provision of credit terms go beyond providing a set number of days to pay for your invoices. It extends to other important sales and payment conditions, including:

- defining how late payments are handled (i.e. late fees);

- outlining a step-by-step escalation pathway for overdue debts (such as reminders, suspension of services, referral to external collection, and potential recovery of collection costs);

- specifying accepted payment types (EFT, Cheques, Credit Cards, PayPal etc);

- providing invoice requirements (i.e. PO numbers or uploading invoice details to client portals);

- detailing dispute delivery timeframes;

- setting out expectations around part-payments or payment plans; and finally,

- including a ‘debt collection costs recovery’ clause.

Documenting these elements in writing, getting them agreed before work starts, and repeating them in engagement letters and invoices turns simple credit terms into a practical credit policy that supports cash flow, reduces disputes, and gives both parties a clear roadmap if something goes wrong.

Tip #3 – Set Credit Limits

If your business sells high ticket items or expensive services on credit terms, setting up credit limits is a fundamental practice to protect your business from financial risk. Establishing a clear “ceiling” on how much a client can owe at any given time, creates a safety net that prevents bad debt from accumulating beyond a manageable level.

A well-managed credit limit isn’t just about restriction; it’s about fostering a sustainable partnership where both parties understand the financial boundaries of the relationship.

Tip #4 – Perform Credit Checks

Performing credit checks during the onboarding process is the first line of defence against insolvency risk and late payments. By vetting a new customer’s financial history before signing a contract, you can identify red flags, such as court judgements, payment defaults, or high-risk credit scores that might otherwise lead to a significant loss. This proactive step allows you to tailor your payment terms to the risk level of each client, ensuring you aren’t unknowingly subsidising a struggling business.

In Australia, there are a number of businesses that can provide credit checks for a reasonable fee. The most notable are: Equifax (formerly known as Veda), Experian, (formerly known as Illion and Dun & Bradsheet) and Talefin. You can also decide to invest in a Debtor Management CRM which includes credit checks features, such as EzyCollect and Creditor Watch.

Stage 2: Invoicing

Whilst you should aim to invoice your customers as soon as possible, you should also be mindful that Australia has specific regulations about invoice timing. An invoice should be issued upon the service is completed, or the goods are delivered.

Proper invoicing moves beyond timing, a thorough invoice lay out setup and the use of the correct technology to issue and track invoices are also paramount to collect payments faster.

Tip #5 – Set up your Invoice Layout Correctly

Your invoice layout should include all the relevant details to ensure your customers can pay you correctly, get in touch with you for any questions, and sent you payment remittances, avoiding unnecessary payment delays.

Key invoice details, include:

Your Organisation Details

Make sure your invoice layout includes all your organisation details:

- Business Name

- ABN

- accounts contact email

- contact number

Invoice details

- Invoice date

- Invoice number

- Due Date (if you can customise the format for this field, make it a larger font and bold)

Service and Items description

The description of your items or services should clearly reflect how these have been advertised or agreed with your client.

If you sell items, make sure the item name, model number and quantity is included in the invoice description.

If you sell services, make sure the description of the service reflects how this service was presented at the time the customer accepted your terms.

For example, if billing hourly, the invoice should specify the total hours and the hourly rate. However, if billing by project milestone or task, never include time tracking data on the invoice (even if you use it internally for costing) to avoid confusing the client.

Your Company’s Banking & Payment Details

The company’s banking and payment details are generally displayed at the bottom of the invoice and should include:

- bank details (account name, BSB and account number);

- a one sentence summary of your payment terms;

- the accepted payment types (EFT, VISA, AMEX etc).

Invoice Layout Requirements for Subcontractors

Invoice Layout Requirements for SubcontractorsTip #6 – Use the latest technology to send invoices

If you’re still manually attaching PDF invoices to Outlook emails, you’re essentially running your business on ’90s nostalgia. Technology has evolved, introducing online invoicing which enables accounting systems like Xero and MYOB to replace these clunky workflows.

Online Invoicing

With online invoicing, the invoice is still sent via email. However, it is sent as a link as part of the email text, not an attachment. When the customer clicks on the invoice link, the invoice opens on the screen, with an option to download the document as a PDF. This online interaction triggers a digital audit trail, tracking all the customer interaction with the online invoice, providing a full audit trail tracking every time the invoice was accessed and downloaded.

Invoice Attachments

You can also attach supporting documents directly with the sale and decide which documents are for internal use only and which are to be included with the invoice, transforming a simple invoice into a full ‘sales pack’

Email Text Templates

Both MYOB and Xero also allow full customisation of your email templates, ensuring your communication remains professional and on-brand. You never want your email text sending an invoice to simply state: “Hello, please find attached your invoice.”

Stage 3: Payments

A sale is not a sale until it gets paid. Your ultimate goal, when managing your Accounts Receivable system, is to reduce the time gap between Sales and Payments (also called the Debtor Ratio) to the smallest denominator.

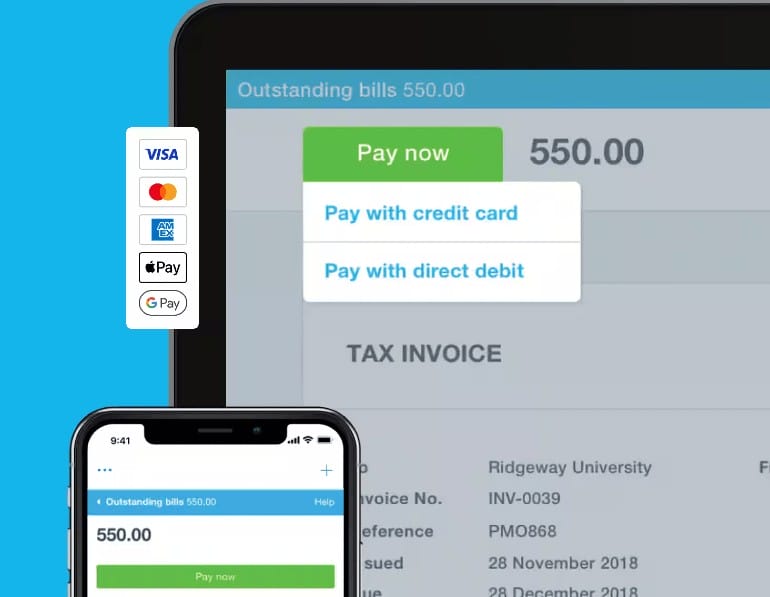

Tip #7 – Increase your payment options

Expanding your payment options is a proven way to accelerate your cashflow, the easier you make it to pay your invoices, the faster the payment occurs.

Whenever possible, phase out obsolete and high-risk payment types like cash or cheques in favour of more efficient digital options.

Wholesalers, Contractors, and Professional Service firms tend to limit themselves to standard EFT transfers, often overlooking Australia’s most popular convenience: credit cards.

By integrating an online payment provider, like Pinch Payments or MYOB PayBy, you can offer both online EFT payments and credit card facilities available directly from the online invoice screen at no extra cost to your business. These systems even handle the automation on-charging the card fees. Pinch even provides the ability to offer both payment plans and Direct Debits.

Stage 4: Payment Follow-ups

You have now transitioned from preventing measures to full debt recovery. Stepping into this stage means that your customer has missed their payment deadline and your cashflow starts being at risk.

Tip #8 – Implement an automated Follow-up Process

To maintain consistent cash flow, you must implement a structured debt follow-up made out by a multichannel approach, blending email, SMS, and direct contact, ensuring maximum impact. For example:

- Gentle Nudge: (email) | 7 Days Overdue

- Formal Reminder: (email) | 17 Days Overdue

- Alert: (SMS) | 20 Days Overdue

- Direct Outreach: (Phone Call) | 30 Days Overdue

- Final Warning: (email or registered mail) | 45 Days Overdue | Customer is on hold

- Letter of Demand: (registered mail) | 60-90 (max) Days Overdue

In the debt recovery stage, time is your most expensive resource. Every minute spent chasing an old invoice is time taken away from billable work. Your goal should be to automate the early stages and only step in personally when “personal escalation” is necessary.

Both MYOB and Xero include invoice email reminder features, where you can schedule multiple email reminders to be sent automatically after a set number of days from the unpaid invoice due date. You can fully customise the template for each email based on the relevant stage of the follow-up process.

More sophisticated systems like EzyCollect and Creditor Watch offer Debtor Reminders and expand the range of communication channels to include SMS and registered mail. These are real Debtor Management CRM systems, that can also interactively track when your customers view the email reminders and allow you to take notes about details discussed over phone calls.

Stage 5: Debt Collection

If all your follow-up alerts and reminders have been ignored, you are now at high risk of facing a bad debt, it’s time to delegate this task to a professional that can help you to recover your debt.

Tip #9 – Engage a reputable Debt Collector

When internal recovery efforts stall, partnering with a reputable debt collection agency is a strategic next step to protect your bottom line.

Ideally, you want to engage a specialist who understands your industry, who can swiftly dismantle the common “excuses” debtors use to avoid payment by addressing them with knowledge and authority.

To safeguard your margins against collection fees, ensure your initial terms of engagement include a “costs of recovery” clause. This provision legally shifts the liability for these fees onto the debtor, ensuring that the cost of chasing what you are owed doesn’t come out of your own pocket.

While the goal is always 100% recovery, sometimes even securing a partial settlement is a win for your liquidity compared to a total write-off.

At this advanced stage, accepting an instalment payment plan is also a viable option. To ensure this doesn’t become another administrative burden, insist on retaining control of the periodical payments via a Direct Debit payment plan arrangement. This is feature is available in Pinch Payments.

Stage 6: Court Proceedings or Bad Debt

Here’s a dark secret nobody wants to know: when a debtor does not want to pay, recovery is virtually impossible!

Tip #10 – What to do with the debt?

Make the right decision based on sound cost-benefit analysis

When all else fails, you find yourself at the ultimate Accounts Receivable crossroad.

Where are you going next? Do you keep trying by escalating the debt to court proceedings, or give up and write off the debt?

At this final stage, you must perform a cold-blooded cost-benefit analysis. Is the debt large enough to justify the legal fees, court costs, stress, and the significant time investment required for court proceedings?

An important step towards making this decision is to understand the rules of your local court. In most Australian states and territories, you can lodge a claim through the Small Claims Court. This pathway allows business owners to represent themselves, avoiding the high cost of formal legal counsel. However, these courts have specific monetary thresholds that limit the size of the debt you can claim.

It is also important to note that a judge issuing an Order of Payment is not a guarantee of restitution; if a debtor remains defiant, you must pursue further enforcement proceedings yourself. While self-representation saves on legal fees, the process is undeniably stressful and offers no absolute guarantee of a successful recovery. If the debtor has no searchable assets or is on the verge of insolvency, “throwing good money after bad” only compounds your loss.

In such cases, the most strategic move may be to write off the balance as a Bad Debt. While it’s a difficult pill to swallow, a formal write-off allows you to at least reclaim the GST previously paid and offset the loss against your taxable income, providing a small measure of financial relief as you clear the slate to focus on more profitable, reliable clients.

Conclusions: Protect your most vital Asset

Debtors are one of your business’s most significant assets. To ensure they remain high-quality, bankable assets, you must integrate a strategy that balances prevention, monitoring, and recovery.

The health of your debtors is a direct indicator of your business’s liquidity. Your Aged Receivables should be reviewed at least once a quarter to identify persistently late payers or unusual trends. This is also the ideal time to clear “phantom debtors”, those erroneous entries that distort your true financial position.

Proactive prevention and early intervention are far more effective than late-stage recovery. Traditional debt collection is time-consuming, emotionally taxing, and has a low success rate. Furthermore, aged or phantom debtors skew your cash flow forecasting, leading to inaccurate investment decisions that can jeopardise your business liquidity.

Finally, remember that continuing to supply goods or services to a non-paying customer is a significant risk. A single large bad debt has the potential to wipe out your annual profit or even put your entire business at risk.

Are you struggling to build a proficient, automated, and reliable debtor management system within Xero or MYOB?

At Evolution Cloud Accounting, we specialise in strengthening your recovery process by integrating sophisticated payment and reminder tools. Let us help you implement a fully automated system and ensure your Accounts Receivable is always on point. Contact us to find out how we can help your business.

Disclaimer

This blog and attached resources are of general nnature, designed for informational and educational purposes only. They should not be construed as professional financial advice for your individual business. Should you need such advice, consult a licensed financial or tax advisor.