Novated Lease: a Guide for Employers and Employees

By Paolo, 13.04.2026

A Novated Lease is an ATO approved workplace benefit where an employer provides their employees the opportunity to purchase a new vehicle by paying it via a salary sacrifice arrangement.

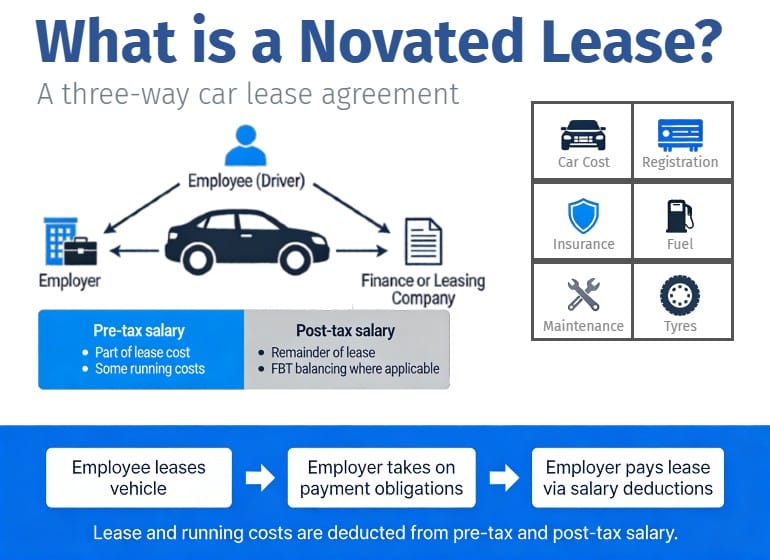

These agreements often extend beyond the initial purchase price to include the vehicle’s running costs, such as registration, insurance, maintenance, and fuel, bundling them into a single payment.

For employees, a Novated Lease agreement helps them reduce their taxable income whilst making easy, predictable repayments for their new vehicles and its running costs.

For employers, Novated Lease agreements are a low-risk employment initiative that can serve as a powerful recruitment and retention tool at zero cost to the company. However, introducing Novated Lease agreements comes with additional administration burdens and compliance requirements that must be properly managed through payroll and HR policies.

A Novated Lease Agreement is a three-way contract between the employee, the employer and the lease company.

Under this arrangement, the employee leases a vehicle, and the employer agrees to take on the payment obligations through salary deductions. The employer then deducts the lease payments and pass them to the lease provider.

Novated Lease Process

- The employee selects a vehicle and applies for finance through an approved provider.

- The employee signs a lease agreement with a finance provider or a bank, which covers the cost of the vehicle (ex GST) and its running costs.

- A novated deed or “Deed of Novation” is signed and executed, transferring the employee’s lease obligation to the employer.

- The employee enters into a ‘salary sacrifice’ arrangement with the employer to cover the car lease repayments from their pre-tax salary and, depending on the vehicle type, their post-tax salary.

- The employer makes repayments to the finance provider on the employee’s behalf using salary deductions from the employee.

- The arrangement continues until the lease ends or employment terminates. If the employee change jobs, they can ask their new employer to transfer the agreement to them. If the new employer does not wish to reprise the agreement, the novation effectively ends, and the lease obligation reverts to the employee, who then resumes payments directly with the finance company (however, these payments change from pre-tax to after-tax).

Frequently Asked Questions for Employers

Is there an obligation for employers to agree to a Novated Lease agreement?

As for any other Salary Sacrifice arrangements (including Super), an employer is under no obligation to endorse a Novated Lease agreement requested by an employee. Employers can also decide to only engage into Novated Lease Agreements with specific groups of employees and not extending this workplace benefit across the entire organisation.

However, should a business decide to introduce Novated Lease agreements in the organisation, a comprehensive Novated Lease policy should first be developed, clearly stipulating the roles, responsibility and liability for each party, to avoid future surprises.

Are there any risks for an employer when offering Novated Lease Agreements?

At its core, a Novated Lease Agreement is risk-free. Although, the employer commits to make the vehicle repayments to the finance company, this is restricted by a clear no wages = no payments rule. If there is no (or insufficient) salary to cover the repayments in a pay period, the employer is not required to “top up” or fund the shortfall. The payment liability shifts immediately to the employee to make the repayments using their personal funds.

The only risks involved is by setting up the Novated Lease deduction into the payroll system incorrectly, or by not keeping the deduction amount up-to-date when the lease provider increases the periodical payments.

Does a Novated Lease involve any direct costs for the employer?

When an employee has a car under a Novated Lease with their employer, the Federal Government considers it to be a fringe benefit. Therefore, depending on the type of vehicle purchased, Fringe Benefits Tax may apply.

While employers are liable to pay Fringe Benefits Tax, in the case of Novated Leases, this cost can legally be passed on to the employee by setting up a second post-tax deduction. This FBT calculation method is called the Employee Contribution Method (ECM) which also spares the employer from registering for Fringe Benefit Tax solely due to this arrangement.

Does a Novated Lease involve any indirect costs for the employer?

Setting up and maintaining Novated Lease agreements require additional administration and compliance tasks, which result into more work for the internal payroll/admin team or increased fees charged by an external accounting/payroll provider.

Does a Novated Lease provide any financial benefits for the employer?

As the employee’s total pre-tax earnings from the wages is reduced, so is the superannuation liability paid by the employer. The employer is required to pay superannuation on the reduced employees’ Gross Wages. The reduced gross wages are also reflected in the calculation of the employer’s Payroll Tax liability.

Does the employer have any responsibility towards the vehicle purchased?

Although, the vehicle registration is made on the employee’s name, the full ownership of the vehicle stays with the leasing company, until the full payment of the vehicle is made by the employee. The employer has no claim, rights or obligations towards the vehicle. The sole role of the employer is to collect the vehicle repayment money from the employee’s pay and pass it to the leasing company.

Does the employer receive any tax relief from the value of the vehicle?

The ownership of vehicles purchased by employees under Novated Lease Agreements is solely between the employee and the leasing company. Therefore, employers should never record the vehicle as a company’s asset, added it to their Asset register, receiving depreciation benefits or input tax credits.

What are the employer’s obligations when it comes to Novated Lease Agreements?

Employer’s Novated Lease obligations are fairly straightforward, and they include:

- Set up and manage the payroll deduction – the lease provider will provide the deduction amounts to set up;

- Timely pay the lease provider – forward the contributions to the leasing provider on time to avoid payment delays;

- Communicate with the lease provider – timely communicate with the lease provider when the employee’s earnings are insufficient to meet the lease amount;

- Accurately report the deductions – correctly report gross wages on: Activity Statements, employees’ Income Statements and Payroll Tax.

What are the compliance requirements applicable to Novated Lease Agreements?

Novated Lease Agreements’ compliance requirements are set out by the Australian Taxation Office. The ATO uses the Novated Lease data-matching program to detect:

| For employers | For employees |

|

|

Novated Lease Payroll Process, Payments and Reporting Requirements

Introducing Novated Lease Agreements requires additional Payroll set up and processing, Accounts Payable and admin tasks.

Setting up and Manage the Novated Lease Deductions

Depending on the vehicle type purchased by the employee, the following Novated Lease Payroll deductions must be set up:

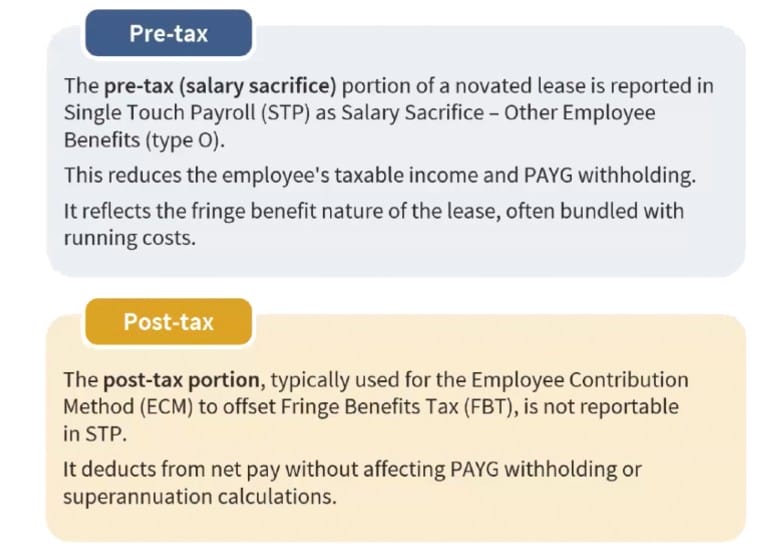

- Pre-Tax (Salary Sacrifice)*: used for the lease and running costs. This pay item must be set up to reduce the employee’s taxable income, PAYG withholding and Superannuation. In STP, it is reported as Other Employee Benefits (Type: O)

- Post-Tax (Employee Contribution Method – ECM)*: used to offset Fringe Benefits Tax (FBT) liabilities. By paying a portion from after-tax income, the taxable value of the benefit can often be reduced to zero, saving the employer from paying FBT. As this is an after tax deduction, this is not reported in STP.

*If the employer covers FBT, or the employee purchases a fully electric vehicle under the Luxury Car Tax threshold for the year, only the pre-tax deduction pay item is required.

When multiple employees take Novated Lease Agreements, the payroll team should consider setting up a specific deduction pay item (and liability account) for each employee or lease provider, or manage the lease reconciliation outside the payroll system using reconciliation worksheets.

Leave & Termination Scenarios

- Leave Without Pay/Parental Leave: The employer should stop or suspend the deductions, inform the employee they must make the lease payment directly to the financier using post-tax dollars until they return, and finally notify the lease provider of the change in circumstances.

- Employment Termination: The “novation” ends immediately. The employee takes the car and the remaining lease obligations with them, either paying directly or transferring it to a new employer.

Making payments to the lease providers

The process to make payments to the lease provider varies depending on the provider. The most common options are:

- Tax Invoice/Direct Debit: the provider will periodically issue a Tax Invoice to the employer and request this signs a direct debit agreement allowing them to automatically withdraw the required funds from the company’s bank account once the invoice is due. For companies with multiple employees on Novated Leases, some providers also issue consolidated invoices covering all participating employees, making reconciliation easier.

- Payroll Alignment: Providers structure the payment schedule to match the employer’s specific cycle, whether it is weekly, fortnightly, or monthly, to ensure deductions and remittances happen simultaneously.

- Automated Data Files: some providers supply “payroll files” that can be imported directly into accounting software such as Xero, MYOB, or QuickBooks, showing the exact pre-tax and post-tax amounts to deduct.

BAS, Payroll Tax, and Workers’ Compensation

- BAS (W1 on Activity Statement): as the pre-tax deduction reduces taxable wages, this reduces the amount reportable on W1 on the Business Activity Statement. The post-tax component does not affect any reportable amount.

- Payroll tax: as the pre-tax deduction impacts the gross wages, this must be deducted from the calculation of the Payroll Tax liability. The post-tax component has no impact on the liability calculation.

- Workers’ Compensation: depends on state jurisdiction, but most include as part of the “assessable wages/remuneration” salary, wages, and most fringe benefits subject to FBT. Therefore, the deduction should not impact the calculation of Workers’ Compensation actual wages.

End of Payroll Year (STP Final Declaration)

Employers must disclose the Reportable Fringe Benefits Amount (RFBA) on the employee’s Income Statements when the grossed-up taxable value exceeds $2,000. This is not taxable income but affects income-tested calculations (e.g., HECS, Family Tax Benefit and Child Support deductions).

Novated Lease Benefits & Requirements for Employees

Vehicle ownership can only be retained by either an individual or a company. Partnerships or Trusts that wish to purchase a vehicle must register it in the Trustee’s name or one of the partners’ names.

Vehicles can be purchased via three different options:

- Outright Purchase: where the vehicle is purchased upfront. This option is available to both individuals and companies and saves the buyer interests and fees. Purchasing a vehicle outright, has no tax benefits and, in particular for companies, this may create a negative equity of an asset that rapidly depreciates.

- Vehicle Loan: The vehicle is purchased either by financing the entire cost of the vehicle or a percentage. Part of the vehicle cost can be offset by paying a percentage upfront, or by trading a previous vehicle. Repayments are made from after-tax income, interest charges and borrowing fees apply. The ability to deduct the running costs of a vehicle vary depending on specific circumstances. This option is also available to both individuals and companies.

- Novated Lease: The vehicle (and its running costs) are packaged into a lease agreement whose repayments are payable via a salary sacrifice arrangement. This option is only available to individuals currently employed as employees.

Each purchase options presents both benefits and costs, as each individual’s financial situation is different, before purchasing a vehicle, individuals or company owners should consult their Accountant or financial advisor to identify the most cost-effective and tax saving options tailored to their specific circumstances.

As the topic of this blog is Novated Lease, we will focus solely on the key benefits and considerations employees should be aware when taking this option.

Buy vs Loan vs Lease a Car

Benefits of purchasing a vehicle with a Novated Lease

GST Savings – Novated leases are goods and services tax (GST) free for employees. The GST the employee would ordinarily pay on the vehicle purchase price is covered by the finance provider. However, GST does apply on the residual value payable at the end of the lease.

Predictable payments deducted even before wages are paid – A novated lease offers predictable payments, as individuals know exactly how much will be deducted each pay cycle. This consistency allows for easier budgeting of repayments, as the fixed nature of the costs removes uncertainty from the financial planning process.

Flexible options and terms – Novated Lease agreements are available for both new and second-hand vehicles. The term of the lease agreement is flexible, to suit the employee.

Personal and Business use – With a Novated Lease, the employee can also use the car for personal use. These arrangements don’t restrict the use of the car exclusively for work or business purposes.

Reduction of Gross Income – The employee’s taxable income is reduced. The car purchase cost and ongoing running costs each year ultimately set how cost-effective a Novated Lease is for the employee.

Purchase and running costs included – The benefits also depend on the way the lease is structured. Some leases may package car expenses such as registration, fuel, tyres and insurance together so the employee’s repayments cover these, too. If running costs are included in the employee’s Novated Lease, these are packaged with the lease repayments.

Considerations for Employees

Purchasing restrictions – Novated Lease providers may impose several limitations on employees purchasing vehicles to manage risk and depreciation. Common restrictions include car age limits, mileage caps (often under 150,000 km), and requirements that vehicles be roadworthy. Additionally, provider approval is required for modifications, with enhancements needing to be installed upfront. Some employers may restrict certain makes, models, or luxury vehicles that exceed FBT thresholds.

Individual Tax Implications – It is important for employees to understand how a Novated Lease, and any associated financial implications, may impact their personal circumstances. As every individual’s financial situation is different, employees are responsible to assess their own financial situation, including the impact on taxable income, HECS debts and other government benefits.

Obtaining advice from employers – Although employers can offer general information about Novated Lease Agreements, they cannot provide advice on whether this is a better purchasing option than other types of vehicle purchase, as this falls under ‘financial advice’.

Liability – Although the employer is responsible to make payments to the lease provider, the ultimate liability to make these payments rests with the employee. This means when their wages are not sufficient to cover the cost of the repayment, or when changing jobs, the employees are still liable to make these payments from personal funds.

Fringe Benefits Tax – Fringe Benefits Tax applies to all Novated Lease Agreements. Although, technically, this tax is the employer’s responsibility, the ATO has provided ways for the employer to pass this liability to their employees. Employees should carefully review their company’s Novated Lease Policy and gain a clear understanding about who will be liable to cover the FBT associated costs.

Superannuation – as Novated Lease payment decrease the employee’s gross wages, the gross earnings subject to Superannuation is reduced accordingly, causing the employee to receive less Superannuation on their wages.

Leave without Pay – Employees are still liable to make their lease repayments during their Leave without Pay periods. The lease provider offers a number of options for employees on unpaid leave, including:

- make direct post‑tax payments to the lease company whilst on leave;

- prepay some or all lease costs before going on unpaid leave;

- temporarily de‑novate (convert to a direct lease);

- permanently terminate/settle the lease, if affordable.

Termination/change of employment – when the employee decides to change jobs, the liability carries over with them. The liability can be taken by the new employer (at their discretion). If not, the employee will need to convert to a direct lease.

End of Lease – at the end of the lease, the employee must pay the residual amount of the vehicle (inclusive of GST) to own the car outright. If the employee does not have the funds to cover the cost of the residual value, they can apply for other financing options, or sell the vehicle privately.

Frequently Asked Questions for Employees

Who owns the vehicle?

Although the car is registered under the employee’s name, the legal owner of the vehicle is the lease provider until the lease agreement is finished, and the residual payment is made.

Is there a minimum salary to get a Novated Lease?

Novated leasing approval is dependent on the employee’s capacity as a borrower, much like traditional finance. This means the employee needs to illustrate their ability to meet regular repayments over the term of the lease.

What is the average length of a Novated Lease?

Novated Lease agreements range between one and five years, the shorter the term of the salary packaging agreement, the higher the residual.

What’s the vehicle’s minimum and maximum value available to an employee?

The maximum amount a person can borrow generally depends on the employee’s annual salary, their capacity to repay, and the lease provider. Minimum Novated Lease amounts are generally between $5,000 and $10,000.

Are there any fees in setting up a Novated Lease?

Depending on the lease provider, setup and origination fees may be chargeable at the start of the lease. Some providers may also include an early exit fee.

What is included and excluded in the running costs?

Inclusive running costs vary by lease provider, they may include: registration, CTP and comprehensive insurance, roadside assistance, maintenance and fuel/electricity charges.

Vehicle fines, tolls and parking are always excluded from the agreements.

Are Novated Lease arrangements available to Company Directors?

Novated Lease arrangements are available exclusively when the Director is set up as a working employee for the company and receives an Annual Salary subject to PAYG. However, Company Directors should always seek advice from their Accountant on the most tax viable option to purchase vehicles.

How much is the residual value payable at the end of the lease term?

Residual vehicle values are generally around 28% – 30% of the total value of the car.

Final Thoughts

Navigating the world of Australian tax and vehicle finance can feel like a maze, but the Novated Lease remains one of the most effective strategic salary packaging tool when managed correctly.

For employers, it enhances remuneration offerings without additional cost. However, to stay compliant, employers should work with experienced payroll consultants to maintain transparent, well-documented arrangements that meet the ATO requirements.

For employees, it offers a simplified way to budget for one of life’s most expensive items by making simple, predictable periodical repayments deducted even before they receive their net pay in their bank accounts.

However, employees need to understand this isn’t a “one size fits all” solution. The impact on HECS, child support, and Government benefits means employees should always look at the full picture, rather than simply focusing on the tax savings.

With the current FBT exemptions for Electric Vehicles, there has arguably never been a more lucrative time to explore this option. But before signing on the dotted line, it’s always advisable to speak with a qualified financial advisor to ensure the numbers align with individual circumstances.

Disclaimer

This blog and attached resources are of general nature, designed for informational and educational purposes only. They should not be construed as professional financial advice for your individual business. Should you need such advice, consult a licensed financial or tax advisor.