How to Manage Leading Hand Allowances in Payroll

By Paolo, 22.06.2026

Managing payroll under Australian Modern Awards can be a complex task, especially when it comes to specific employee entitlements. One of the most common additions to an employee’s pay packet is the Leading Hand Allowance, a mandatory payment designed to compensate employees who take on extra supervisory responsibilities while remaining “on the tools”.

Understanding how to calculate, report, and tax this allowance is critical to staying compliant with the Fair Work Ombudsman and the Australian Taxation Office (ATO).

We have developed a comprehensive guide to navigating Leading Hand Allowances for Australian employers. In this blog, we answer common questions and clear any doubts that Employers often have towards managing this Allowance.

What is a Leading Hand Allowance, and how do I know if I have to pay it?

Under Fair Work Ombudsman guidelines, a Leading Hand Allowance is payable when an employee is given the responsibility of directing and supervising the work of other employees

- Mandatory requirement: for all employees who are officially assigned supervisory duties;

- No senior title needed: the employee does not need a manager title to qualify; overseeing the actions or productivity of other staff is enough.

- On-the-tools supervision: it typically applies to workers who perform their normal daily labour alongside minor supervisory tasks.

How do I calculate the Leading Hand Allowance for my staff?

The Allowance calculation method is dependent on the Industrial Instrument. The calculation method generally falls into two categories:

- Fixed Dollar Amount: a flat rate paid either per hour, day, or week;

- Percentage of a Standard Rate: a percentage calculated against the “standard rate” specified in the Award, which is often the weekly base rate of a specific classification level rather than the employee’s actual pay rate.

The allowance amount also increases depending on the number of workers the employee supervises during a shift or roster period. Commonly, the Allowance amount splits across the following brackets:

- 1 person

- 2-5 people

- 6-10 people

- Over 10 people

What happens once I nominate an employee to receive this payment?

Paying the allowance solidifies a formal operational shift in the employee’s workplace role.

The appointment and rate should be documented in writing, including the number of persons in charge, to substantiate the classification tier being applied.

- Clear Expectations: define their extra responsibilities, such as coordinating tasks, enforcing safety rules, or tracking team output;

- Continuous Assessment: monitor the highest number of team members they supervise during a shift, as a temporary surge in team size can bump them into a higher allowance bracket for that period;

- Revocation of Duty: if operational needs change, their supervisory responsibilities are formally removed, employers can cease paying the allowance, provided it is handled in accordance with contract terms and award conditions.

Am I required to withhold PAYG Tax and pay Superannuation on this allowance?

Leading Hand allowance is fully integrated into standard payroll tax and super obligations.

- PAYG Withholding: applies to this allowance exactly as it was part of gross wages;

- Superannuation: because supervising staff forms part of the employee’s regular duties, this payment is classified as Ordinary Time Earnings (OTE)/Qualified Earnings (QE) and is subject to Superannuation Guarantee (SG).

Is the Leading Hand Allowance deemed assessable or exempt for Payroll Tax?

The Leading Hand Allowance must be included as part of the assessable wages in the Payroll Tax Annual Declaration across all states and territories, as it forms part of gross wages.

Do I need to include Leading Hand allowance in my Workers’ Compensation Actual Wages calculations?

As this allowance is deemed part of Ordinary Time Earnings, it must be included in the calculation of actual wages when submitting the annual Workers’ Compensation Actual Wages Declaration across all states and territories.

How do I report this allowance through Single Touch Payroll (STP Phase 2)?

Under ATO STP Phase 2 rules, Leading Hand Allowances must be reported as a Task Allowance (ATO Code: KN) because it relates to a specific duty or responsibility.

The Leading Hand Allowance must be “disaggregated” from the base rate (configured as a separate pay item) in the payroll system when submitting the payroll data to the ATO via STP.

Although, under STP rules, the Leading Hand Allowance is reported the same way across all Employment Agreements, the Industrial Instruments classify this allowance differently. In some Awards/Agreements, this allowance is deemed as an All-purpose Allowance, whereas in other Awards the Leading Hand Allowance is deemed as a Standard Allowance.

This is a significant difference, especially when it comes to pay the Leading Hand Allowance when the employee is either not managing a team or absent on leave.

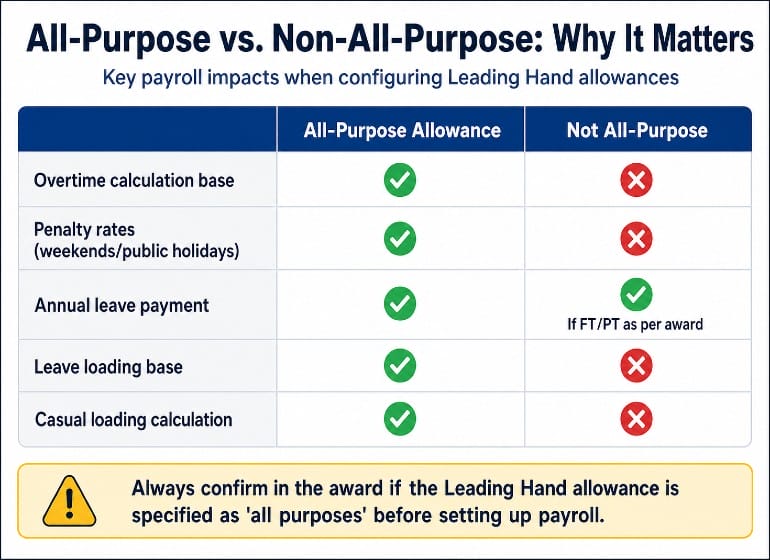

What are the core differences between an “All-purpose” and “Standard” allowance?

The distinction dictates how this allowance interacts with other wage calculations like overtime and penalties. The core principles between the two classification types are:

- All-purpose Allowance: the allowance is “packaged” with the employee’s base hourly rate. This means the allowance becomes an integral component of the employee’s pay rate, therefore influencing the calculation of overtime, shift penalties, paid leave, and public holidays.

- Standard Allowance: the allowance is treated as a separate, flat addition to the pay packet. It does not boost the base rate used when calculating penalty rates, or when paying leave entitlements.

Specifically, the different classification determines the following:

1. Whether the Leading Hand Allowance is paid for all hours worked, or only when the employee actively performs leading duties:

- All-Purpose Allowance: as it is permanently integrated with the employee’s base rate, it must be paid for all hours worked.

- Standard Allowance: it only applies during the hours or days the employee is actively supervising staff.

2. Whether the Leading Hand Allowance is paid when an employee is on leave:

- All-purpose Allowance: the allowance must be paid while the employee is on annual or personal/carers leave.

- Standard Allowance: generally, it is only paid for the actual shifts the employee is at work, actively executing those duties. However, some Awards/Agreement will specifically require the employer to pay it when a worker, who generally takes supervisor duties, is taking Annual Leave. Therefore, employers should carefully review the provision of their Employment Agreement to ensure the payment of this allowance is managed correctly for employees on Annual Leave.

3. Whether the Leading Hand Allowance is paid on (Non-Worked) Public Holidays:

- All-purpose Allowance: it is paid on public holidays.

- Standard Allowance: it is not included with the public holiday rate.

Do I have to pay the allowance when another employee takes over the role for a single day or shift whilst the team leader is away?

Under most Fair Work modern awards, the Leading Hand allowance is based on the tasks actually performed, not just an official job title, therefore when a worker takes over these duties for either a single or a number of shifts, this worker is entitled to receive the Leading Hand allowance whilst covering a supervisory role.

Conclusion: Staying Compliant with Confidence

Managing Leading Hand Allowances doesn’t have to be a source of payroll stress.

Employers should follow these core steps to ensure this allowance is treated correctly within their organisation:

- Always check how the classified Industrial Instrument treats the Allowance: whether this is treated as “all-purpose” or “standard” as this impacts the calculation of penalty rates, leave entitlements and public holidays.

- Correctly map the Allowance for STP, and always ensure both PAYG and superannuation are calculated when setting it up in the Payroll System.

- Check how the Allowance payment is structured in the classified Industrial Instrument (fixed amount or percentage) and ensure different pay item are set in the payroll system for each team size bracket.

- Because missing a bracket upgrade or miscalculating leave entitlements can quickly lead to underpayment claims, regular audits of the team structures and payroll configurations are highly recommended.

Struggling with understanding how to set up and manage your payroll based on the complexity of your Award or Enterprise Agreement?

With a solid 15 years experience in training payroll, small business accounting systems, configuring and managing payroll systems for medium-sized businesses with teams ranging between 5 and 100 employees, Evolution Cloud Accounting is the perfect partner for your business to ensure you are never entangled into risky and expensive compliance issues.

References

https://masterbuilders.com.au/construction-award-changes-what-you-need-to-know

Disclaimer

This blog and attached resources are of general nature, designed for informational and educational purposes only. They should not be construed as professional financial advice for your individual business. Should you need such advice, consult a licensed financial or tax advisor.