Navigating PAYG Instalments: A Guide for Australian Businesses

By Paolo, 23.03.2026

PAYG Instalment is a tax liability reportable on the Activity Statement. Although, this is the third most common tax liability reportable in the BAS (preceded by GST and PAYG Withholding), this is generally the tax that raises more questions and concerns from business owners.

If you run a business, you may have come across PAYG instalment and wondered why the ATO requires its payment. While it can seem confusing at first, PAYG instalment is a forward-thinking system to help a business manage its Income Tax bill gradually, avoiding a large sum at the end of the Financial Year, which can put an incredible strain on the business cash resources.

In this article, we’ll explore the concept of PAYG Instalment, helping you understand how your business performance and evolving income streams may trigger this obligation. We will also address the most frequent questions business owners ask their BAS and Tax Advisors, to ensure you gain a clear understanding on how this tax liability works.

1. What is PAYG Instalment?

PAYG instalment (PAYG-I), or “Pay As You Go Instalment”, is an advancement of the business forthcoming income tax paid throughout the Financial Year in your Activity Statement. The instalment amounts paid during the year are offset against the final tax assessment. The ATO uses this advance instalment system to help businesses manage their tax obligations throughout the year, instead of paying one lump sum at tax time.

2. I have several businesses set up as different entities, all of them are profitable, why do I pay PAYG Instalment for some entities and not others?

PAYG Instalment is a prepayment of Income Tax. Therefore, this tax liability applies exclusively to Companies (Propriety Limited) and individuals. As the Company is deemed by the ATO as an independent taxable entity, it is the only business structure required to pay PAYG instalment as a tax liability.

Other structures, like Trusts and Partnerships (generally) do not pay Income Tax themselves; instead, they pass their profits through to their beneficiaries or partners. Consequently, these entities do not have PAYG instalment obligations.

Finally, for Sole Traders, the tax obligation sits with the individual, not the business. This means any PAYG instalment notice received must be recorded as a personal tax bill, even its income derived exclusively by the business.

When a business covers the cost of a personal PAYG instalment by paying it through its bank account, this payment cannot be coded as a business liability. The correct recording method varies depending on the business structure:

- Sole Trader: Record as Drawings;

- Partnership: Record as the relevant Partner’s Drawings account;

- Trust: Record as the relevant Beneficiary’s Loan account;

- Company: Record as Director’s or Shareholder’s Loan account.

3. How will I know if I have to pay PAYG Instalment?

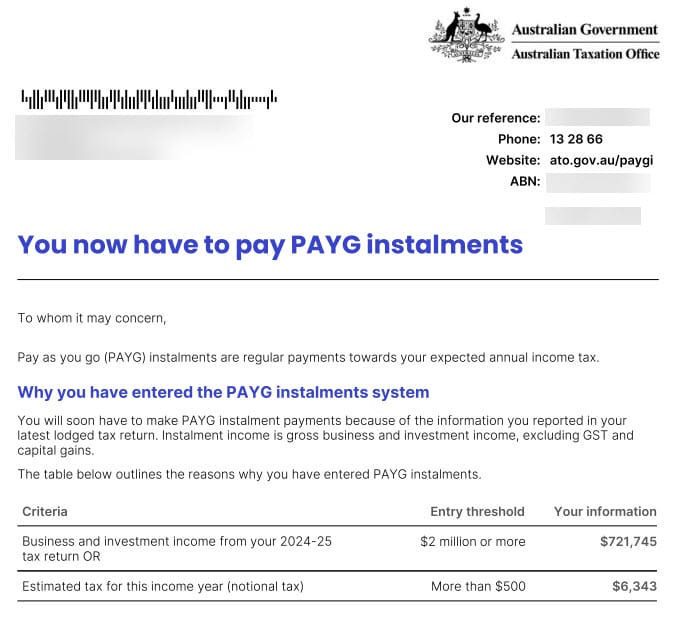

The ATO automatically triggers the registration of PAYG Instalment when the first positive Tax Return has been lodged, and the business or individual exceeds the following thresholds (as of FY 2025-2026):

Individuals

PAYG instalment registration is triggered when the individual meets ALL of the following:

- Instalment income (gross business/investment income, ex‑GST and CGT) of $4,000 or more on the latest tax return;

- Tax payable on the latest notice of assessment of $1,000, or more;

- Estimated (notional) tax of $500, or more.

Companies

PAYG instalment registration is triggered when the Company meets ANY of the following:

- Instalment income from the latest tax return of $2 million, or more;

- Estimated (notional) tax of $500, or more;

- The company is the head company of a consolidated group.

The ATO will notify the business, as well as any BAS/Tax Agents linked to the business, that PAYG Instalment will be included in the next BAS. The notification may come by post or electronically, depending on the communication settings set out on the ATO Business portal.

Both businesses and individuals also have the option to voluntarily register for Pay As You Go (PAYG) Instalment. The registration can be processed both by the Business via their MyGov Account or by their Tax Advisor. The ATO also provides a Pay As You Go Instalments calculator to assist businesses in determining the correct instalment amount to pay the ATO (a separate PAYG Instalment calculator for individuals is also available).

It is highly recommended that businesses seek advice from their Tax Advisor before registering, PAYG instalment payments may not be necessary even if the business is generating a profit in the Financial Year. The Accountant may utilise previous years’ accumulated losses to offset the current income, effectively recording a loss for tax purposes.

A Sample Letter of the ATO PAYG Instalment Auto-Registration Notice

4. In my BAS I noticed I am required to pay both PAYG Instalment and PAYG Withholding, am I paying PAYG twice?

What’s the difference between PAYG-I and PAYG-W?

The term PAYG means “Pay as You Go”, and the ATO generally refers this term to Income Tax. “Pay as you Go” means that the income tax is paid in advance as the taxpayer earns its income.

Therefore, if the trading entity is deemed a Tax Payer (i.e. a Company), PAYG Instalment is payable as an advance of the company’s income tax estimated from the latest lodged Tax Return.

Businesses who employ staff are also responsible to withhold their employee’s estimated Income Tax from their Gross wages and pass it to the ATO through the Activity Statement. Therefore, PAYG Withholding is an advance of the employees’ Income Tax, based on their individual tax circumstances provided when completing a Tax File Declaration. Employers simply withhold the estimated tax from their employees’ gross pay and pass it to the ATO. This becomes the accumulated income tax paid in advance by any individual taxpayer who works as an employee.

At the end of the Financial Year, when these employees (or their Accountant) lodge their Tax Return, the ATO will calculate the actual Income Tax and deduct the amount of PAYG withheld from each periodical pay. The individual will either:

- receive a refund of Income Tax > if the PAYG paid during the year exceeds the total declared Income Tax; or

- will have to pay additional income Tax > if the PAYG is less than the Income Tax declared.

5. How often do I have to pay PAYG Instalment?

While tax liabilities like GST and PAYG Withholding can be reported monthly, PAYG Instalments for companies cannot be reported more frequently than quarterly. The ATO cannot accommodate for monthly variations.

For those businesses who manage their cash flow monthly, they can manually prepay 1/3 of the estimated instalment to the ATO Activity Statement account for the first two months. When the quarterly BAS is lodged, they’ll only need to cover the remaining balance, together with the full payment of the other tax liabilities.

Whichever way a business chooses to manage PAYG Instalment, it’s essential not to dismiss it. Smart business owners don’t just see their quarterly PAYG instalment notice as a last-minute bill at BAS time. They factored this liability directly into their cash flow forecast, turning a potentially large debt into a predictable, routine cash outflow.

Additional planning options also include allocating a percentage of each sale invoice and transfer it to a dedicated tax savings account. Business owners can rely on real-time reporting from their accounting system, to monitor their taxable income.

6. What is the difference between Option 1 and Option 2, and how often can I switch between the two?

The ATO provides two payment options.

Option 1 – the ATO calculates a fixed instalment amount based on latest Income Tax return lodged. This option provides certainty, as the instalment amount remains the same for each period until the next Tax Return is lodged.

Option 2 – the ATO calculates a percentage to apply to the business quarterly income declared in the Activity Statement. This option is more suitable for those businesses whose income varies significantly during the year, such as Farming or Hospitality businesses with seasonal income fluctuation.

Ultimately, choosing between option 1 and 2 depends on the business type, industry, cashflow and income forecast. The percentage rate method offers a self-adjusting payment, while the fixed amount gives the business certainty.

A business can choose between the two options once a year, upon lodging the first Activity Statement of the Financial Year (July–September).

| Calculation Method | Description | Suitable for |

| Option 1: Instalment Amount | A fixed quarterly amount set by the ATO based on the latest lodged Tax Return. | Businesses with steady, predictable income. |

| Option 2: Instalment Percentage | A percentage, provided by the ATO, applicable to the business quarterly income. | Business with variable or seasonable income fluctuation. |

7. If I select Option 2 (% of income), what income is the PAYG-I calculated on?

The assessable income used to calculate the PAYG Instalment amount is based on the BAS reporting method.

If the BAS reporting method is set to Cash, the assessable income is based on the invoice payments received during the quarter, as the Cash method excludes any unpaid invoices.

If the BAS reporting method is set to Accruals, the assessable income is based on all the invoices issued during the quarter, regardless of their payment status.

The easiest way to calculate the PAYG Instalment rate is by taking the income declared on the G1 field on the Activity Statement. If the amount declared in G1 includes GST, then this amount must be divided by 1.1 to calculate the net assessable income, where to apply the PAYG Instalment rate.

8. If I select Option 1 (instalment amount), why does the instalment amount suddenly changes in the middle of the Financial Year?

PAYG instalment amounts are assessed based on the most recently lodged tax return and a predetermined uplift factor to account for inflation. As Companies have until the 15th of May to lodge their previous year’s Tax Return, the PAYG Instalment amount may vary substantially if the latest assessed Income Tax is significantly different from the Tax lodged the previous Financial Year.

PAYG Instalment can also significantly reduce for the same reason. If the Income Tax assessed over the latest Tax Return for a business is already less than the PAYG Instalments amount paid over the quarters of the Financial Year, the PAYG Instalment for the remaining quarters will automatically reduce to nil.

If the latest Tax Return reports a loss or no longer meets the PAYG-I threshold, the ATO will automatically remove the business obligation to pay PAYG instalments, until the next positive Tax Return is lodged.

| Example 1 – ATO Variation of PAYG Instalment

FY 2023-2024

FY 2024-2025

|

9. Can the PAYG Instalment be reduced if I am struggling with my income/cash flow?

If so, who should I contact to seek advice?

If the business income is expected to be lower than in previous years, or the business is struggling financially, it may be possible to vary the PAYG instalment to better reflect the current financial circumstances, assist with cash flow management and prevent tax overpayments.

The Tax Agent is the person solely responsible to assess Income Tax (and therefore the PAYG Instalment payable). Even if the BAS Agent or the business owner is responsible to lodge the Activity Statement, the specific instructions to reduce the PAYG Instalment must always come from the Tax Agent.

However, as many Tax Agents only review the company’s financial annually, a proactive BAS Agent who is responsible to manage the everyday accounts, should reach out to the Tax Agents, and encourage them to review the current business financial situation to potentially reduce the PAYG Instalment.

PAYG-I variations should be made with care. If instalments are reduced too significantly and the varied instalments are less than 85% of the total income tax payable at the end of the year, the ATO may apply interest and/or penalties.

Therefore, any PAYG-I variation should be properly reviewed based on assessable and supportable projections.

When the Tax Agent approves the PAYG Instalment variation, they should also provide the person responsible to lodge the BAS, the following information:

- The varied PAYG Instalment amount or percentage

This amount/percentage should be the result of the current and forecasted profit and cashflow situation for the business. - The revised estimated Tax payable for the year

The estimate Income Tax payable for the year is an important piece of information to be provided by the Tax Agent who has calculated the varied amount. The ATO may reject the BAS if the proportion between the estimated Income Tax payable for the year and the varied amount don’t match. Entering the estimated Income is not as straightforward as some people may think (see example 2 below). - The Reason code to justify the variation

The ATO only allows a reduction of PAYG Instalment based on the following reasons:

21 – Change in investments: The business sold assets (like shares) or changed investment strategy, meaning they’ll have less investment income than the previous year.

22 – Current business structure not continuing: The business has stopped trading, been sold, or is undergoing liquidation.

23 – Significant change in trading conditions: External factors, such as new competition or major restructuring costs, have reduced the business profit margin.

24 – Internal business restructure: An internal expansion or contraction that significantly lowers the expected Income Tax.

25 – Change in legislation or product mix: New laws or a shift in the products the business sells have impacted the business taxable income.

27 – Use of income tax losses: The business’ Tax Advisor plans to use previous years’ tax losses or capital losses to offset this year’s income.

| Example 2 – Estimated Income Taxable Payable for the Year

The Kids’ Centre is a small Childcare located in Sydney and set up as a Company. Based on the FY 2024-2025 Tax Return, the ATO has set a PAYG Instalment payable amount of $2,500 per quarter. The July-September 2025 BAS was lodged with $2,500 PAYG Instalment payable. In October 2025, the business had to close one of their rooms because of a leakage. Due to this damage, the business suffered an income downturn. The Tax Advisor revised the income received from October 2025 and provided Jane, the business owner responsible to lodge the BAS, a revised PAYG Instalment of $500 per quarter for the remaining 3 quarters of the Financial Year. They also provided reason code 23 – Significant change in trading conditions to use as a justification of the PAYG Instalment reduction. However, the Tax Advisor omitted to provide the estimated Income Tax payable for the year. Jane attempts to lodge the Oct-Dec BAS by entering the following details:

The ATO rejects the BAS lodgement, claiming the proportion between T8 and T9 is incorrect. This is because the ATO expects 50% of the tax instalment to be paid by the December BAS. Therefore, in this instance, Jane should have calculated the Estimated Tax for the year as follows: $2,500+500 = $3,000 * 2 = $6,000. |

10. Can I just pay what tax I owe the ATO when I lodge my return and not bother with PAYG instalments?

Once the PAYG Instalment registration requirements are met by the business (or individual), the quarterly PAYG Instalment requirement is mandatory and cannot be opted out.

11. What happens if, at the end of the Financial Year, I have paid more PAYG Instalment than my Income Tax for the year?

The ATO will report a credit in the business Income Tax Account. Interest credits may also be included.

The Tax Agent can choose to:

- Initiate a refund of the Tax credit (and interest) to be paid into the business’ nominated bank account; or

- Transfer the Tax Credit to a different ATO Account (for example, the Activity Statement account) to cover all or part of another current or future tax liability.

12. Where in my Financial Reports can I see the total accumulated PAYG Instalment amount I paid during the Financial Year?

PAYG Instalment is a Balance Sheet account. However, the interpretation on where in the Balance Sheet this amount should show varies depending on the BAS/Tax Agent who has structured your Chart of Accounts and designed the Balance Sheet.

PAYG Instalment can be interpreted as an advance payment of a liability that does not yet exist and therefore be shown in the Assets section of the Balance Sheet, grouped with other Prepayments, or even in the Debtors section.

Alternatively, it can be interpreted as an advance of a liability that will be generated once the Tax Return is lodged and be shown in the Liability section of the Balance Sheet with a negative balance.

Some BAS/Tax Agent may include both the PAYG Instalments and Income Tax, payable at the end of the Financial Year, in one account.

Others may set up two separate accounts:

- PAYG Instalment > records any prepaid PAYG Instalment for the current Financial Year;

- Income Tax Payable or Taxation > includes the Income Tax Payable for the previous Financial Year/s, as reported on the ATO Income Tax Account (ITA).

Although, both interpretations are valid, it is crucial that both BAS and Tax Agent agree with one structure and remain consistent in coding these transactions.

Conclusion

Managing tax doesn’t have to be a burden; by understanding the PAYG Instalment system and budgeting these quarterly liabilities effectively, your business can effectively utilise PAYG instalments to prevent a large, unforeseen tax lump-sum debt.

Key points about managing this liability correctly, include:

- Always choose the payment option (fixed amount or percentage of your income) based on your business type and cash flow predictability. This option is available once a year when you lodge the first BAS of the year;

- The amount of the instalment is calculated by the ATO using your last lodged Tax Return as a guide. If your Accountant lodges a Tax Return at any point during the Financial Year, the PAYG-I amount/percentage is revised and reflected in the next Activity Statement;

- Your business can only report PAYG Instalment quarterly to the ATO through your Activity Statement. However, if your business manages cash flow monthly, you can voluntarily pay 1/3 of the PAYG Instalment monthly to the ATO;

- If your business is struggling, consult your Tax Advisor to assist you with reducing the amount of PAYG Instalment set out by the ATO;

- All instalments paid during the year are credited against your final Tax Assessment.

– If your income Tax is more than the PAYG, you need to pay the balance to the ATO by the Income Tax deadline.

– If you’ve overpaid your assessed Income Tax at the end of the year, a credit of the overpaid tax, plus interest, is generated in your ATO Income Tax Account. You can choose to have this credit refunded or use it as to offset other current or future liabilities.

Finally, it’s important to stay on top of your ATO obligations and avoid common mistakes, including:

- Missing BAS Lodgement Deadlines

Neglecting your quarterly reporting can lead to unnecessary ATO fines and interest charges, which can quickly eat into your profits. - Overlooking your Instalment Rate

As your business fluctuates, so should your tax. Failing to adjust your rate to reflect your current performance may lead to a debt or overpayment. - Neglecting Cash Flow Preparation

Neglecting to include PAYG Instalment as part of your cash flow forecast, will impact your Cashflow projections.

At its core, mastering your PAYG obligations is an act of financial empowerment. Don’t allow key mistakes like neglecting your quarterly PAYG Instalment to jeopardise your company’s financial health. If staying organised is a struggle, Evolution Cloud Accounting can help you streamline your obligations, maintain compliance and prevent expensive errors.

References

https://business.gov.au/finance/tax/pay-as-you-go-payg-instalments

https://iorder.com.au/publication/Download.aspx?ProdID=75372-04.2025